These are one of the things in my life that I can’t believe my own brother and sister would do to me. Falling for a trap like this made me think that BLOOD IS NOT THICKER THAN WATER. When our mother died, all of us were scrambling on what she has left for us and they discovered this: her Cocoplans Investments.

I was pretty naive about how these things actually worked, so when my older brother and sister stepped in, I fell for the “we’ll handle everything” routine. They basically convinced me that they’d do all the grunt work to get the money processed faster and that “I wouldn’t have to lift a finger”—the cash would just show up in my hands. Even though something felt off and I was skeptical, I let them take the lead because I didn’t think I was “smart enough” to navigate the paperwork myself.

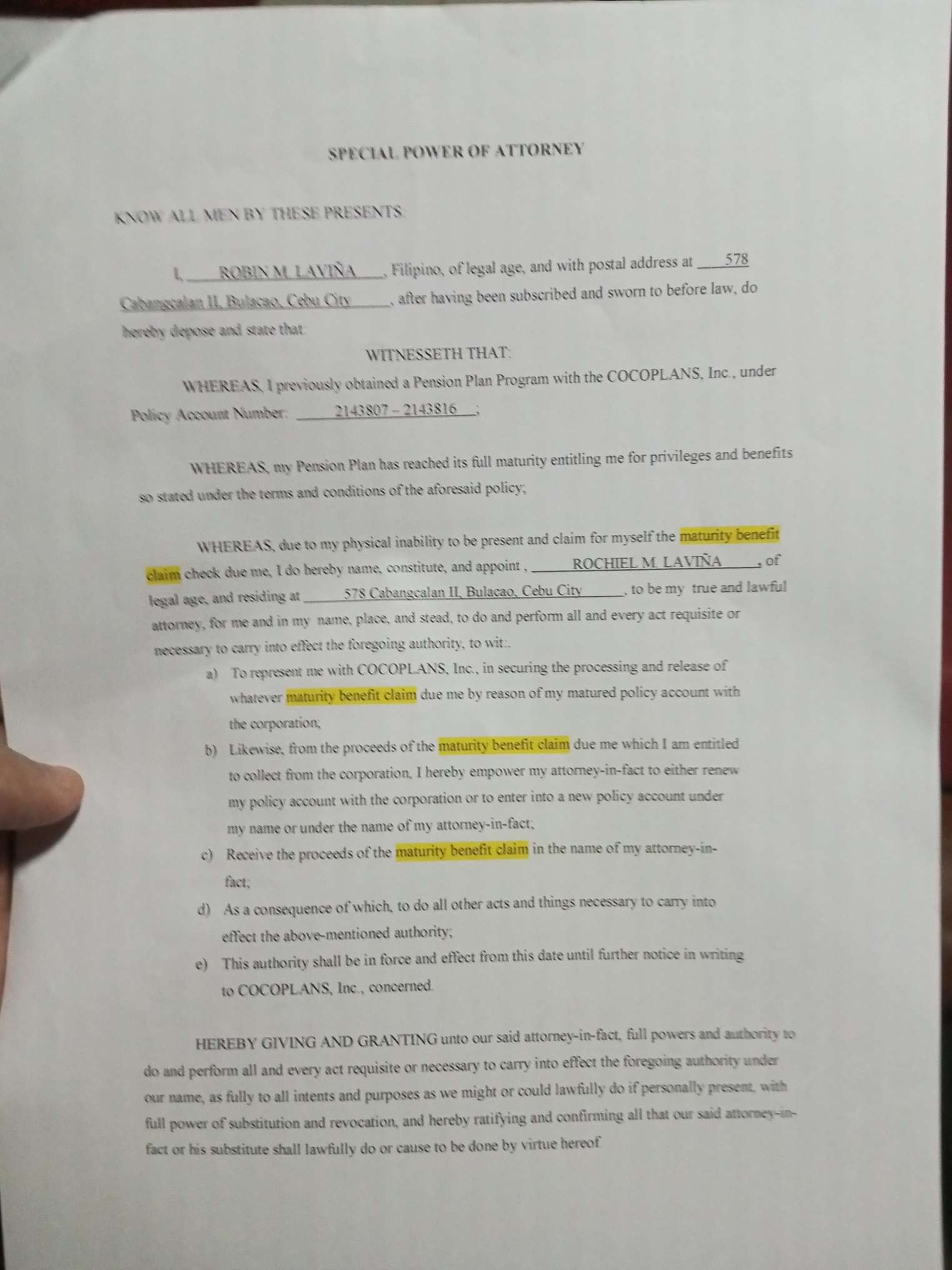

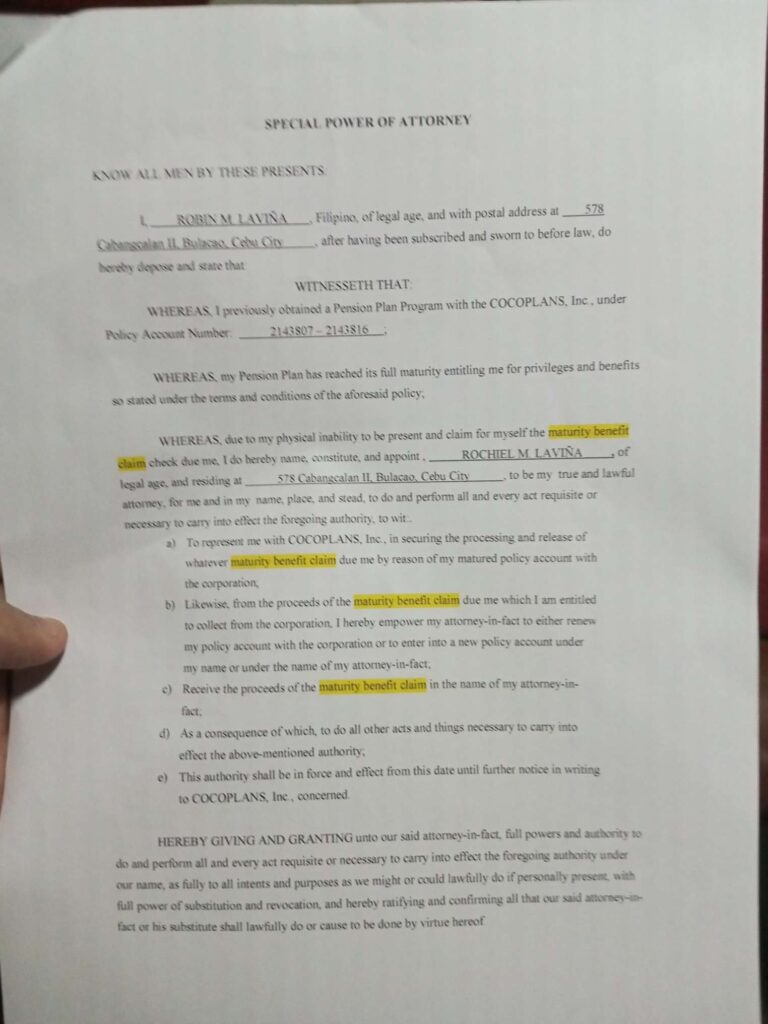

The Special Power of Attorney

Here’s the breakdown of the document they had me deal with:

- The Parties: It’s a Special Power of Attorney (SPA) that makes Rochiel M. Laviña (older brother) the attorney-in-fact, acting on behalf of Robin M. Laviña (younger brother/me).

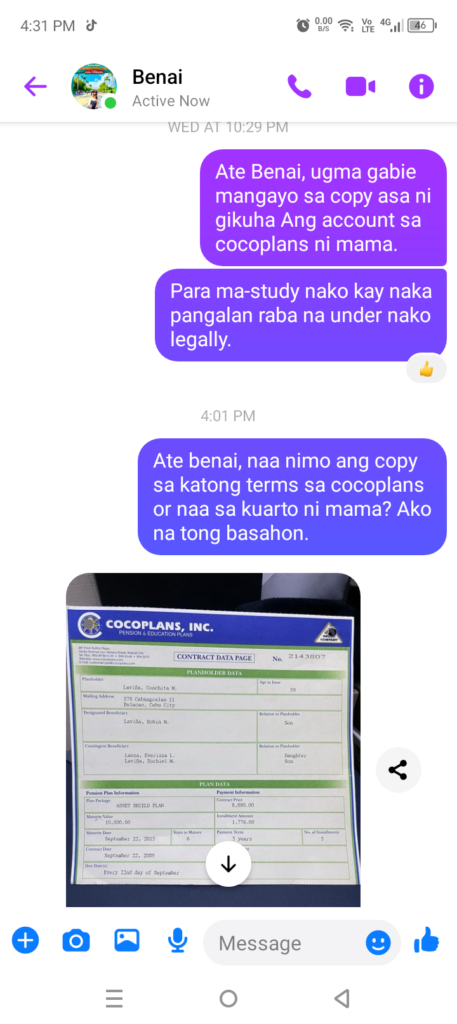

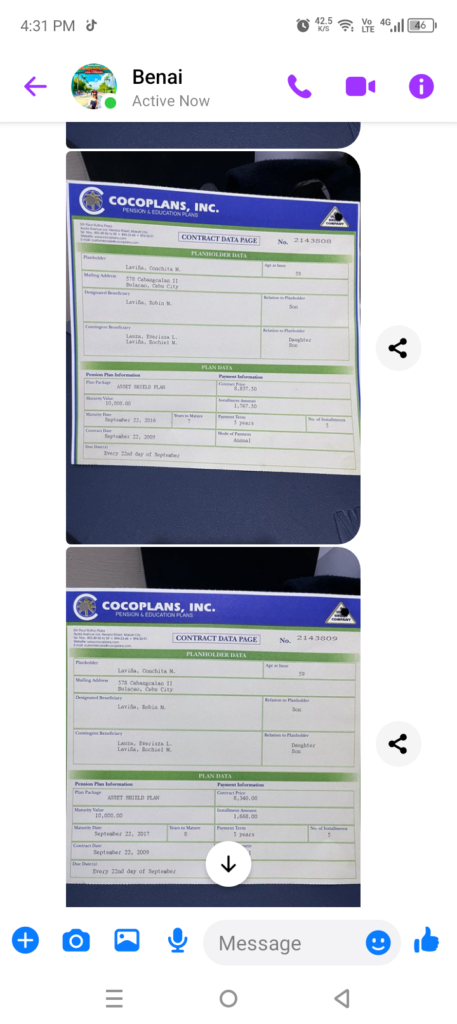

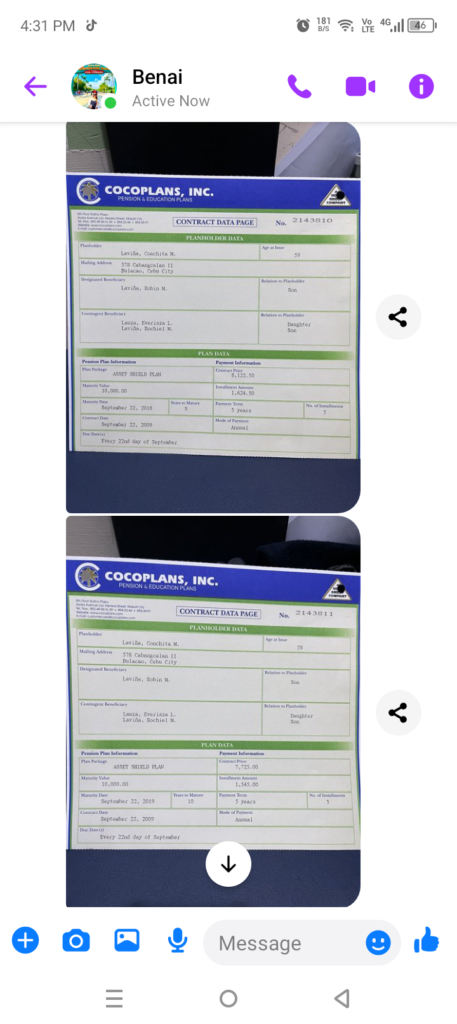

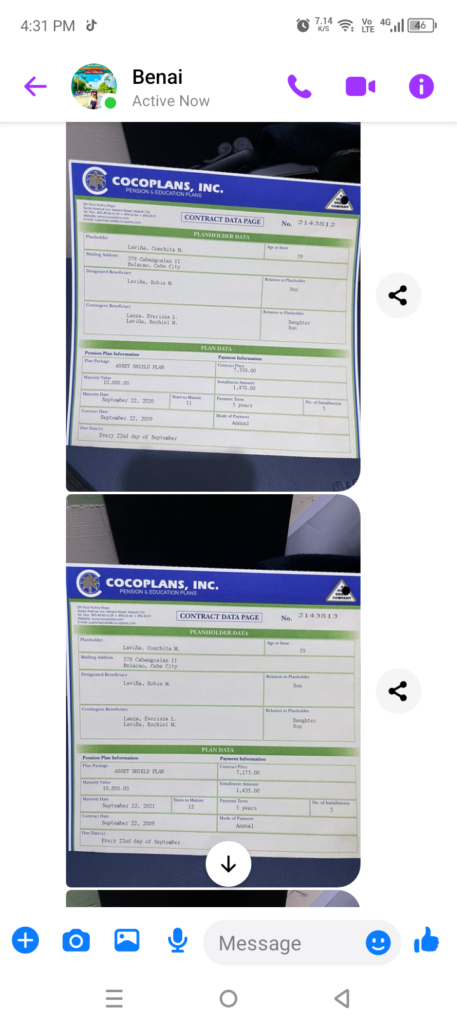

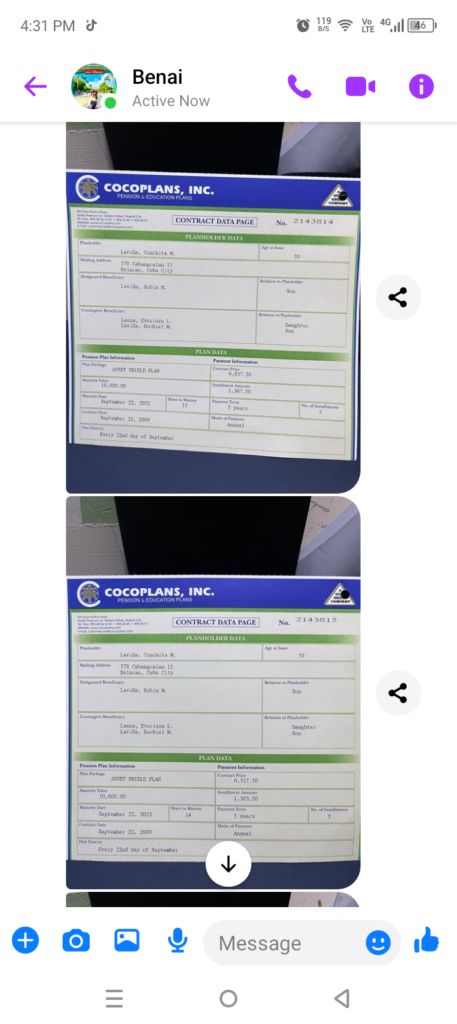

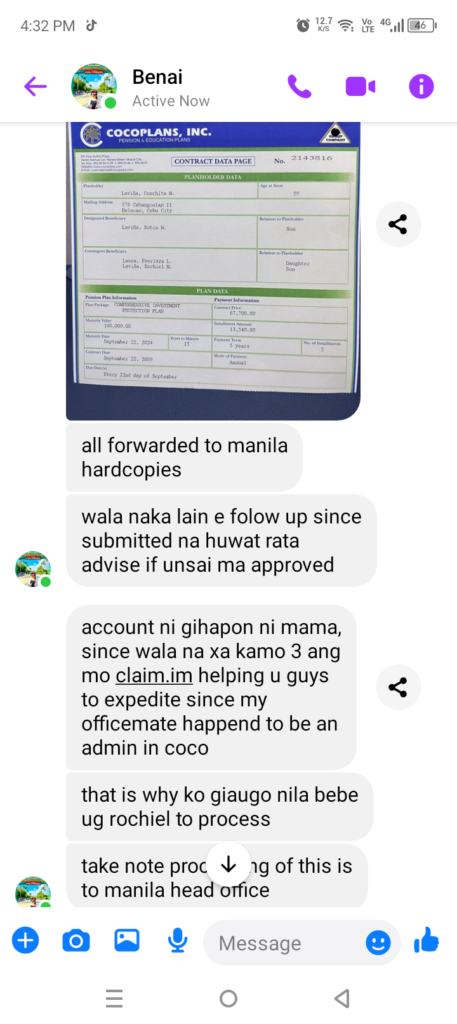

- The Goal: It’s for a matured pension plan at COCOPLANS, Inc. (Policy #2143807-2143816).

- The Reason: It claims I’m “physically unable” to show up, which is the excuse used to let him take over.

- The Powers: This gives Rochiel (older brother) the right to process the claim, sign the papers, and—most importantly—receive the money. It even lets him renew the policy or open new accounts in his name.

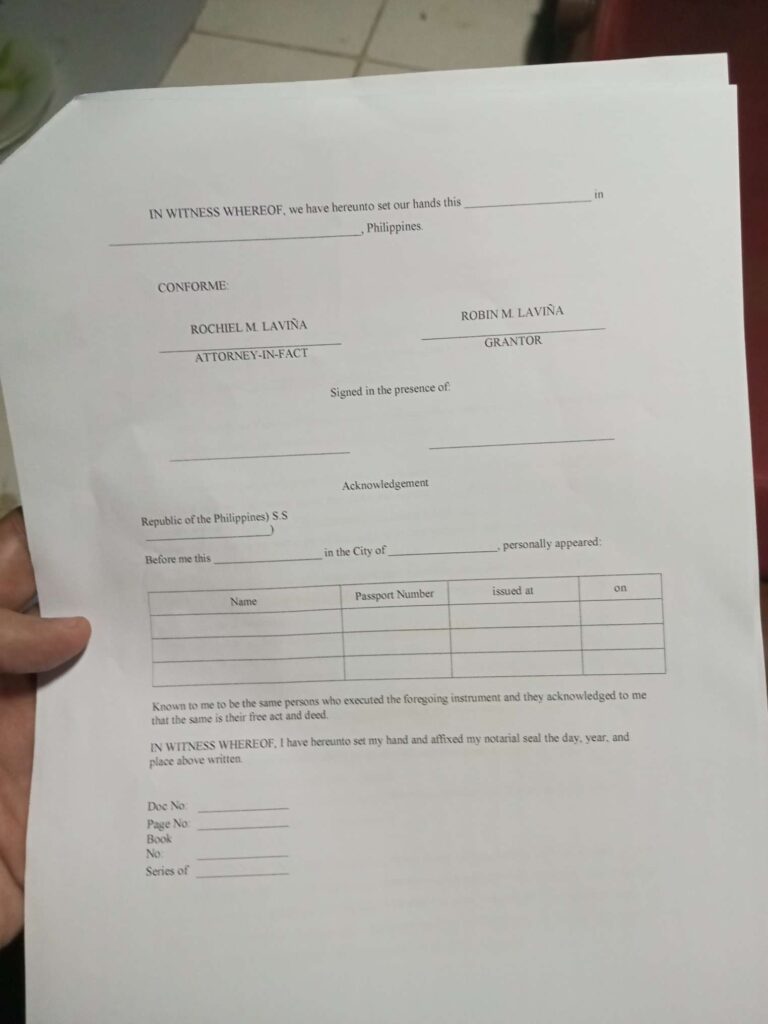

- The Final Step: The second page is just the standard Philippine notary section where we’re supposed to sign in front of a lawyer to make the whole thing official. Which didn’t happen because I signed the paper first before him. The only witness to signing the document was his girlfriend.

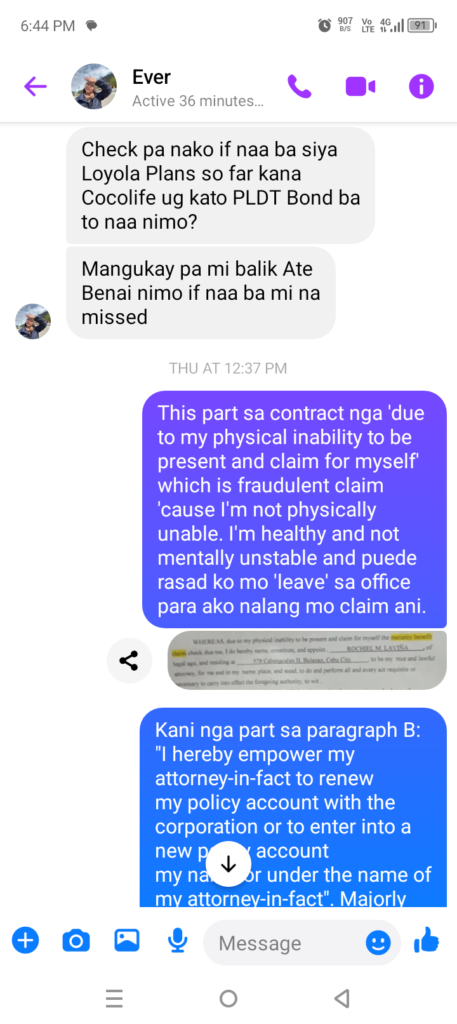

This Special Power of Attorney (SPA) is a legal instrument executed to authorize Rochiel M. Laviña (older brother) to act on behalf of the principal, Robin M. Laviña (younger brother/me). The document identifies the subject as a matured Pension Plan Program with COCOPLANS, Inc., specifically under Policy Account Number 2143807-2143816. The primary justification cited for this delegation of authority is the principal’s physical inability to be present at the establishment to claim the maturity benefit check.

Under the terms of this document, Rochiel M. Laviña is designated as the attorney-in-fact, granting him the specific power to represent the principal in all processing and release stages of the claim. The authority includes the power to receive the proceeds, renew the policy, or enter into a new account agreement under either the principal’s or the attorney-in-fact’s name. The instrument concludes with an acknowledgment section requiring signatures from both parties and witnesses, intended for formal registration before a Notary Public in the Republic of the Philippines.

The suspicious part of the papers…

I think it’s NOT LEGALLY VALID because:

- I didn’t sign it in front of a Notary Public to swear it. Which I think makes it illegal and irregular.

- Because the document explicitly claims I might have a “physical inability” to be present, highly irregular shortcut may have been taken to get a notary to approve it without me being there.

Older Sister Messenger Chat Logs

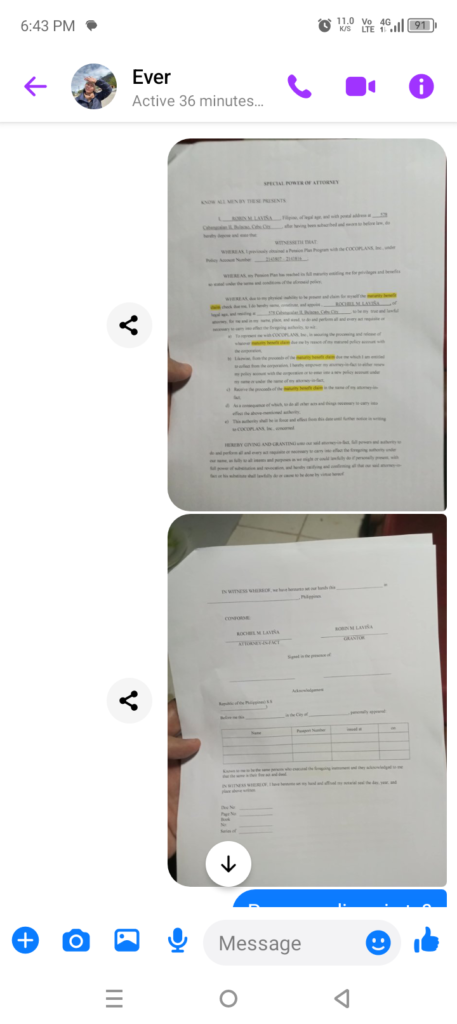

I directly confronted her by sending a screenshot of the Special Power of Attorney (SPA) that they had me sign. I specifically called out the clause that claimed I was granting this power due to “physical inability” to be present, labeling it a fraudulent claim. I made it very clear to her that I am healthy, mentally stable, and more than capable of taking leave from my office to handle my own claims personally.

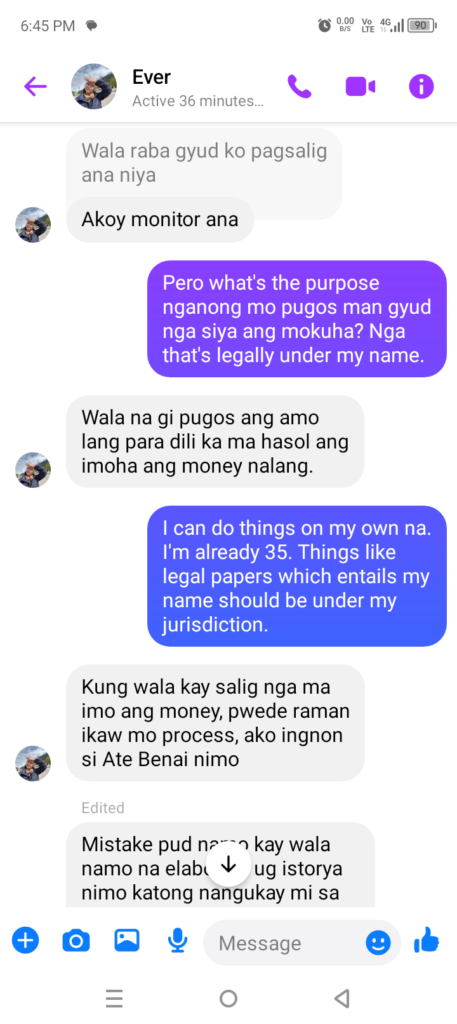

Also asked my sister, Everisza, what exactly I had signed, as I was becoming suspicious of the situation. She attempted to justify the signature by explaining that they have a claim available under our mother’s name at Cocoplans, and they were simply processing it so we could eventually find out the total amount. She framed it as a helpful step, promising that she would update me on the specific numbers once they were available.

However as stated in the Contract Data Page, I am the Designated Beneficiary and they’re just Contingent Beneficiaries.

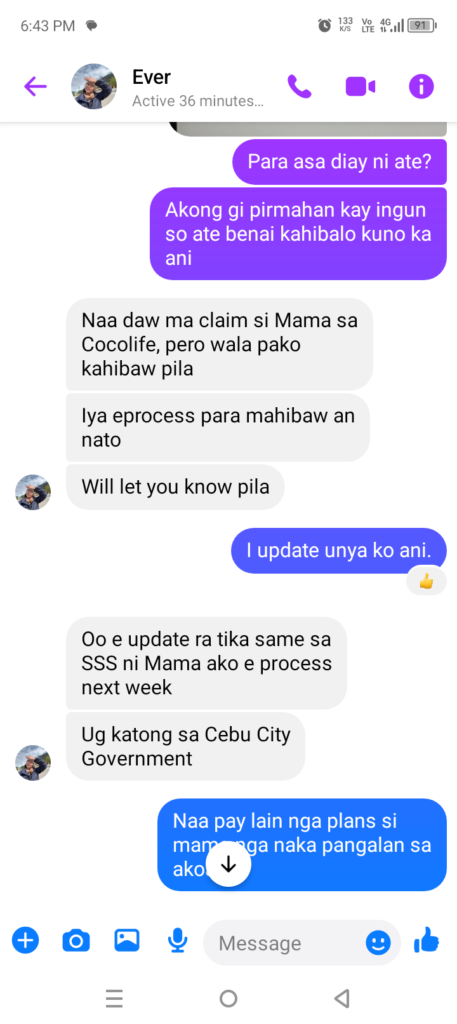

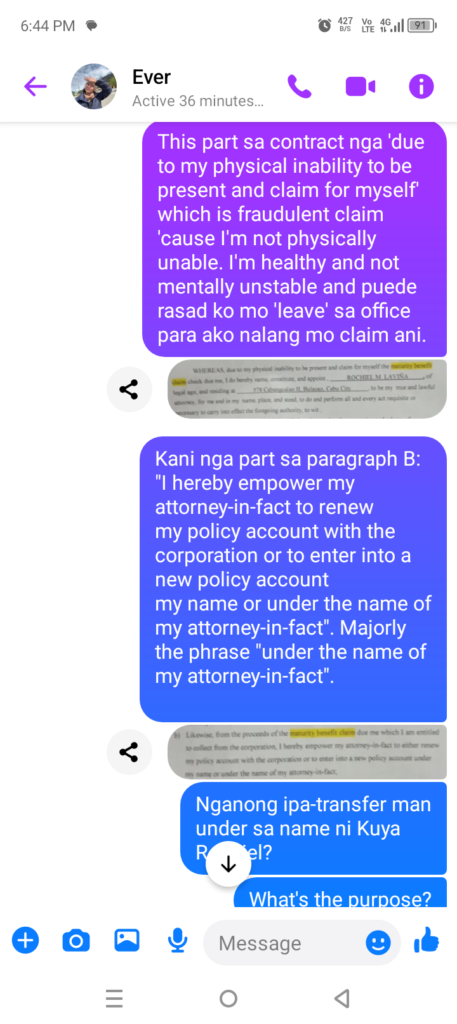

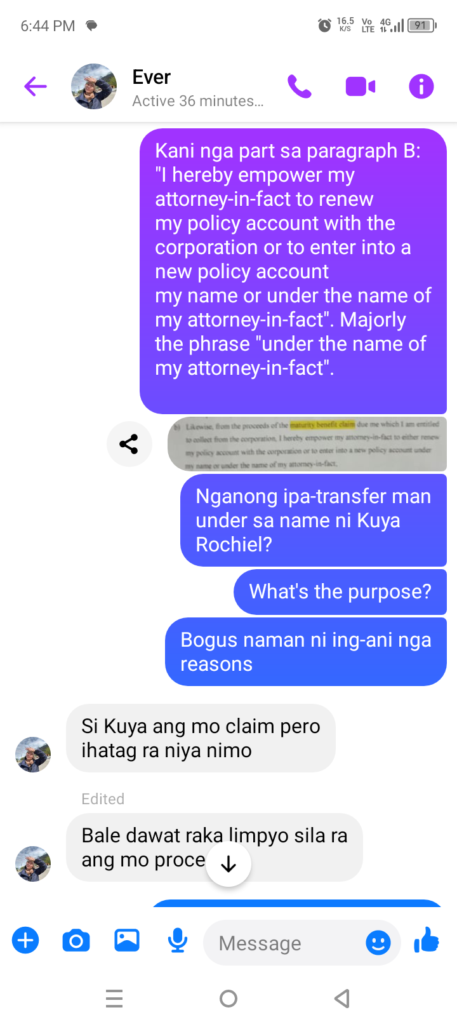

My skepticism grew when I highlighted Paragraph B of the document, which surprisingly empowers my brother, Rochiel, to renew or even open new accounts “under the name of my attorney-in-fact.” I pointedly asked her why my money would need to be transferred into my older brother’s name and what the actual purpose was behind that. To me, the reasons they were giving for this specific arrangement seemed completely bogus.

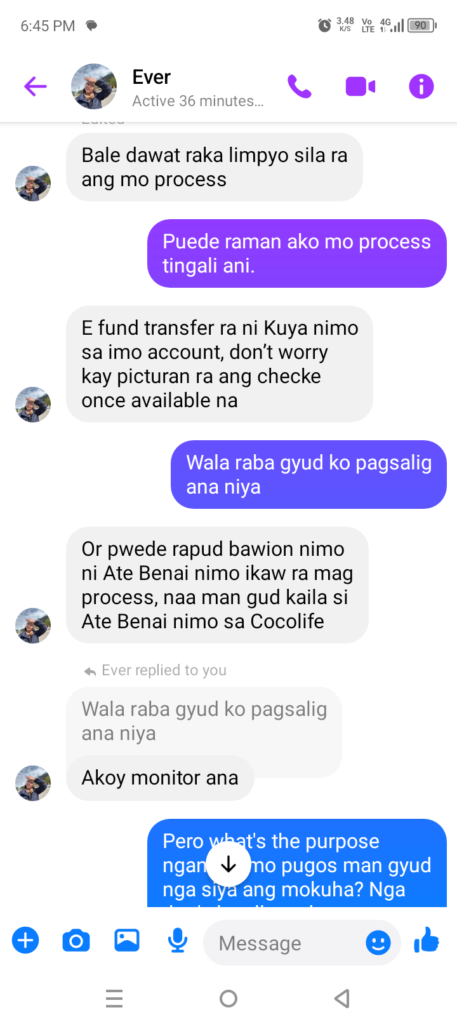

Everisza responded by trying to soothe my concerns, downplaying the legal weight of the transfer by claiming that even if my brother claimed the funds, he would just “give it to you.” She leaned heavily on the idea that they were doing the hard work so I could just “receive it clean” without the hassle of the bureaucracy. It felt like a deliberate attempt to use my perceived lack of experience with these processes to keep me from looking too closely at the paperwork.

I stood my ground and told her plainly that I didn’t trust this arrangement or my brother’s involvement in this specific way. I reminded her that I am already 35 years old and fully capable of managing my own legal affairs. Since these documents and the money they represent are legally under my name, I insisted that they must remain under my own jurisdiction and control.

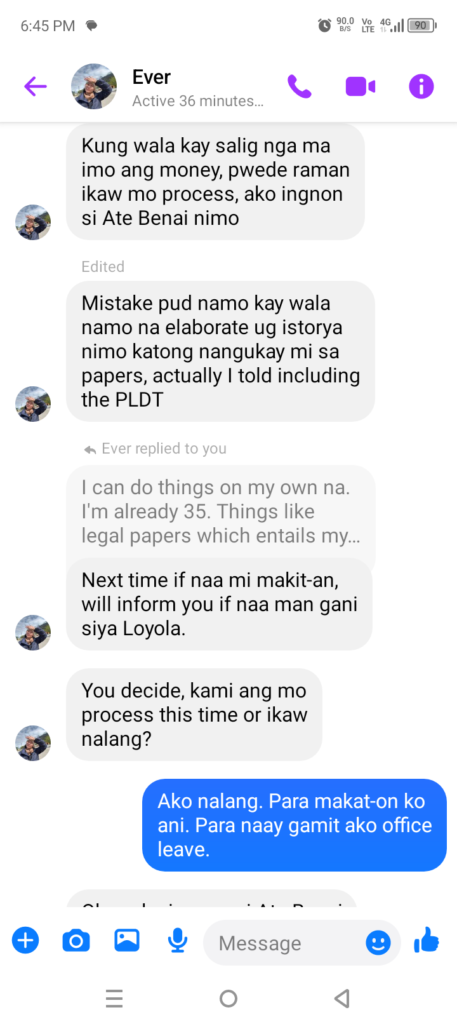

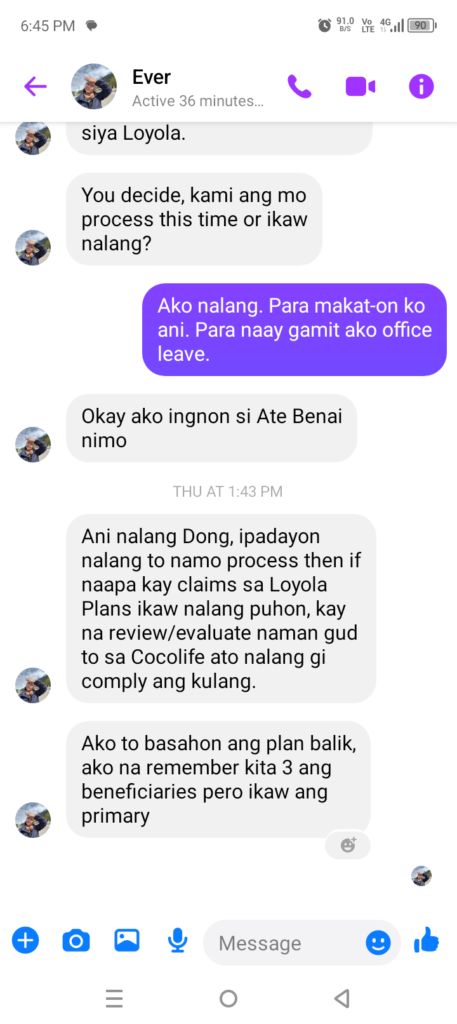

After I pushed back, Everisza initially seemed to fold, agreeing that she would tell Benai to let me handle the process. However, she quickly pivoted and began pressuring me to let them continue, arguing that since they had already started and “complied” with the missing requirements for the Cocolife/Cocoplans claim, it made more sense for them to just finish it. She tried to compromise by suggesting that I could just handle any future claims that might turn up, like the Loyola plans. But, I still highly doubt this claim.

Despite acknowledging my legal priority, she still maintained the narrative that they should be the ones to complete the current process, leaving me feeling like my status as the owner of these accounts was being sidelined.

Contacting Cocoplans Headquarters via Email

Most of my encounters in their branches was a full waste of my time. It was around October 11, 2024. I don’t remember much but I went first to the SM City Cebu branch; I asked their front desk about the plans by showing them pictures. They tried contacting someone but they referred me to another branch in MSY Tower.

At MSY Tower, the only thing I remember was going to a certain upper floor and got to ask some questions with another one of their front desk attendants. The attendant was browsing through some lists on papers, informed about some details I can’t recall anymore, but the person just gave me contact numbers of people to call in. It was a bummer to be referred again to another person in charge. They handed me phone numbers to contact someone Headquarters.

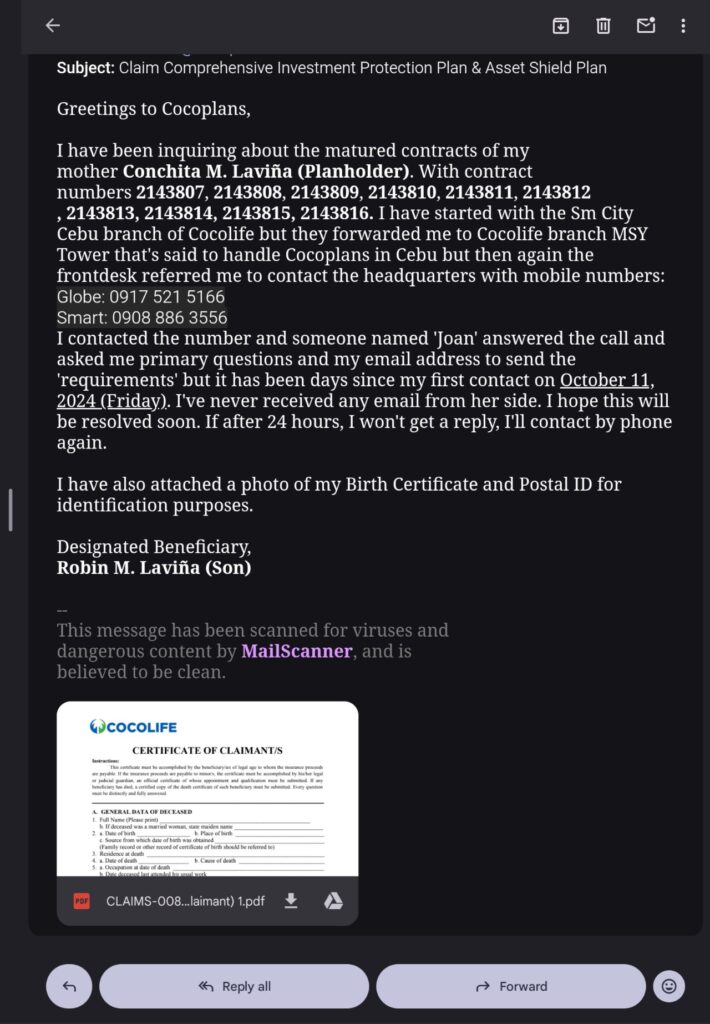

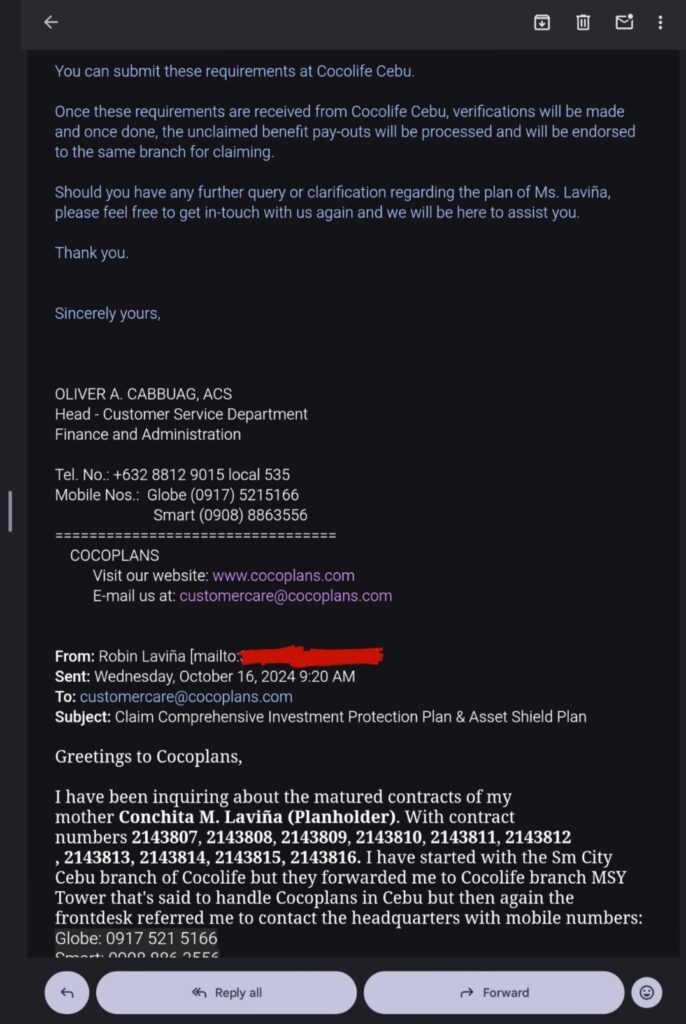

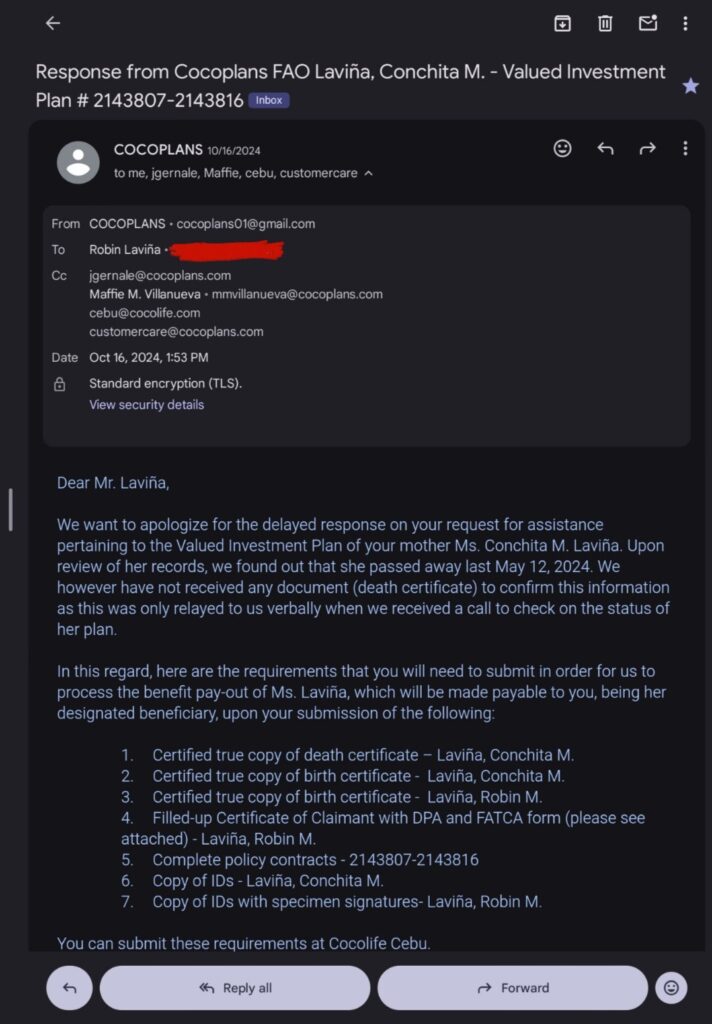

I reached out to the Cocoplans Customer Service Department on October 16, 2024, to finally get some clarity on my mother’s matured pension plans. In my initial email, I expressed my frustration after being bounced between their local branches in SM City Cebu and MSY Tower without getting clear answers. I explained that while I had already spoken with a representative named Joan, I was still waiting on the official list of requirements needed to move forward with the claim for Policy Nos. 2143807 through 2143816.

The response I received from the Head of Customer Service that same afternoon was a major turning point, as it provided official confirmation of my legal standing. The company explicitly stated that the benefit pay-out would be made payable directly to me, formally recognizing me as the sole designated beneficiary on record. They also noted that while they had verbal information regarding my mother’s passing in May 2024, they required formal documentation to officially update their records and begin the disbursement process in my name.

Had to think about the information I got that someone already had

contacted them. They also mentioned specifically that the plans are specifically made payable to me.

The email then laid out a strict list of seven requirements that I needed to submit to the Cocolife Cebu branch to finalize the claim. These included certified true copies of both my mother’s and my own birth certificates, her death certificate, and the original policy contracts. They also required me to fill out a Certificate of Claimant and provide valid IDs with specimen signatures. One BIG problem during that time—I didn’t have my mother’s Death Certificate yet because it was available at the PSA. I was there and they told me it would take more months before it gets processed.

Have you noticed something about the email?

They used a GMAIL ACCOUNT and not their own mailbox using their registered domain names (cocoplans.com and cocolife.com). That to me was already highly suspicious. I still have the copy of this email.

The Cocoplans Cashout

Remember their statement in the email that they arranged for the plans would only be made payable to me? IT WAS ALL BUT A LIE.

I am so dismayed how Cocoplans treats their clients. They didn’t even try to contact me first if the Special Power of Attorney that they received was approved by me. That’s one of the big reasons why I feel like this whole debacle has money paid under the table.

I was shocked that my sister presented me checks in my brothers name.

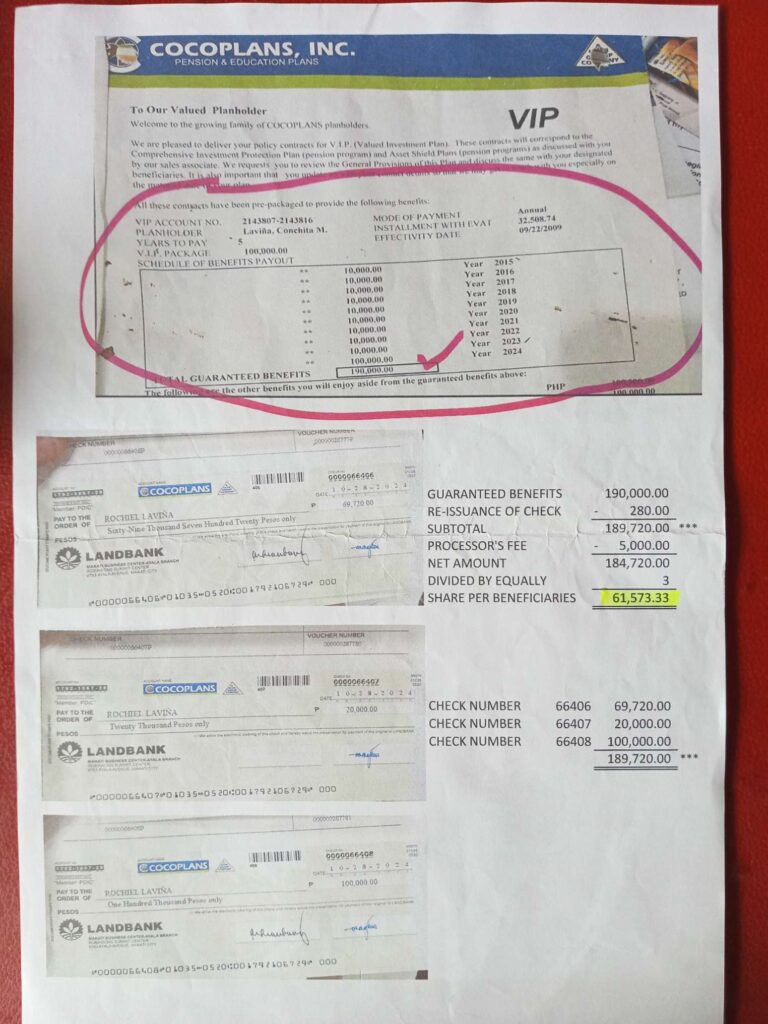

The total amount resulted in a total guaranteed benefit of ₱190,000.00. Lots of fees was deducted which left a net amount of ₱189,720.00 remained. Although I am documented as the sole Designated Beneficiary on every single one of these contracts—which legally entitles me to the full amount—the situation was handled behind my back. Instead of respecting the legal beneficiary designation, they created a calculation sheet that forces an equal three-way split, leaving me with only ₱61,573.33.

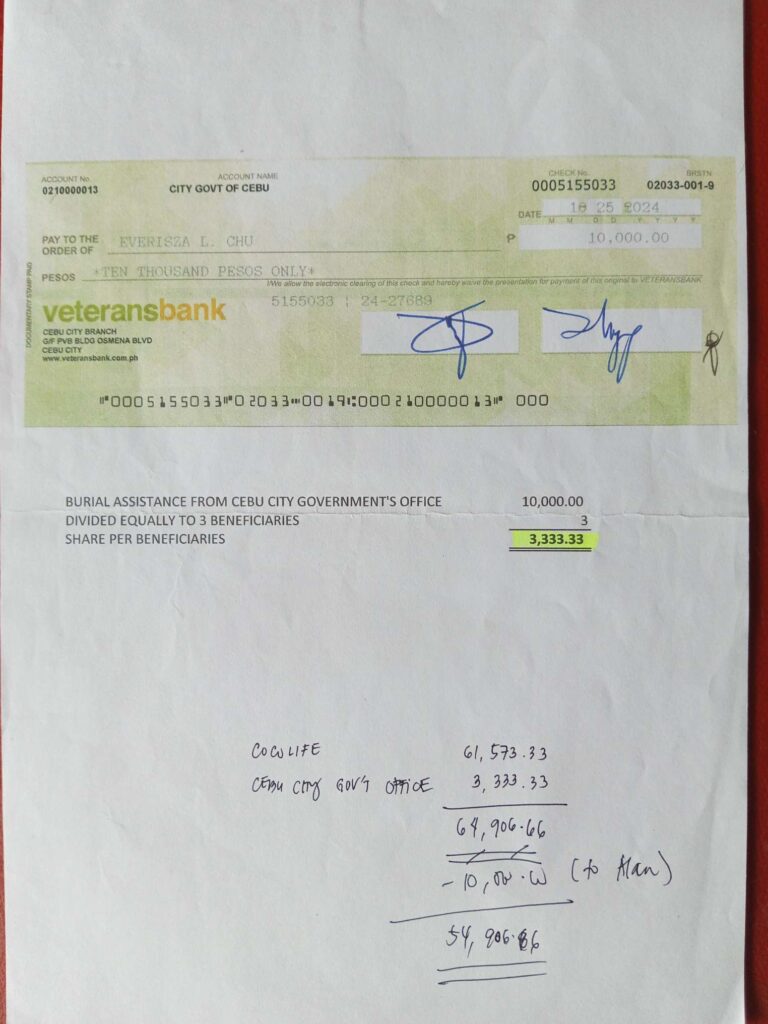

There is also this burial claim. This claim was filed through the Cebu City Government’s burial assistance program following my mother’s passing, resulting in an approved payout of ₱10,000.00. Just like the pension funds, this ₱10,000.00 was split evenly into three portions of ₱3,333.33 each.

The documents indicate that the actual check for this assistance was issued directly to my sister, Everisza.

These are some questions I always had in my mind:

- Was there a need to deduct ₱10,000.00? She claims that I need to pay Alan (her husband) some money. Which is also something I did not agree upon. This is an outright scam.

- Instead of ₱64,906.66 ending up in my hands. I only got to have ₱54,906.66.

- Why are they doing this? I’m for sure they don’t want to treat me equally. Maybe they’re egoists and they feel the need to put me down when they have a chance.

Why I wasn’t able to process after the email contact

Crazy things happened after my mother passed away. She left me a debt of real estate taxes that I have to pay because I’m the one living and maintaining the property which amounted to around ₱50,000.00.

And too many things to handle: Work and paying the debt. All very stressful.

Terminologies

- Planholder: The individual who originally purchased and owned the insurance or pension policy. In this case, the planholder is Conchita M. Laviña.

- Designated Beneficiary (Primary Beneficiary): The person or entity first in line to receive the benefits or proceeds of a policy upon the death of the planholder.

- Contingent Beneficiary (Secondary Beneficiary): The person or entity designated to receive the benefits only if the primary beneficiary is deceased, cannot be located, or refuses the inheritance at the time the claim is made.

- Maturity Benefit: The amount of money paid out by the company (COCOPLANS, Inc.) when the policy reaches its full term or “matured” date.

- Attorney-in-Fact: The person authorized to act on behalf of another person (the Principal) under a legal document like a Special Power of Attorney.

Hierarchy of Rights: Who holds the most right?

When it comes to the inheritance of a deceased parent’s policy, the Designated Beneficiary holds the primary and superior right over all other claimants, including contingent beneficiaries.

In my specific situation regarding the COCOPLANS documents:

- The Designated Beneficiary is Robin M. Laviña (younger brother/me). Because I’m alive and capable of claiming the benefit, I have the exclusive right to the proceeds. Legally, the company is obligated to pay the funds to me.

- The Contingent Beneficiaries are Everisza L. Lavina and Rochiel M. Laviña. Their rights are “contingent,” meaning they only exist as a backup. Since me (the primary beneficiary) is active and claiming my right, the contingent beneficiaries legally have zero claim to the money under the current circumstances.

In the eyes of the law and the financial institution, the Designated Beneficiary is the “owner” of the claim. The presence of contingent beneficiaries does not grant them equal footing or the right to bypass the primary beneficiary’s authority.

Realization

I should have studied Law at my younger years. Because of me being naive about this type of situation that I’ve lost a lot of money.

If you think my brother and sister are in need of money more that I do? No, they’re already well off. They have enough money to travel and enjoy things in life. Which I always question “Where does their source of money come from?” while I slave away my life at a low paying full-time job.

Note: This blog post is my own public documentation and will be updated if there’s any correction needed.

Leave a Reply